The Sustainability Assurance Landscape – An Overview

The landscape for sustainability reporting and assurance is undergoing significant transformation, driven by coordinated initiatives from the UK Government, the FRC, and the FCA. Here's what you need to know.

Background

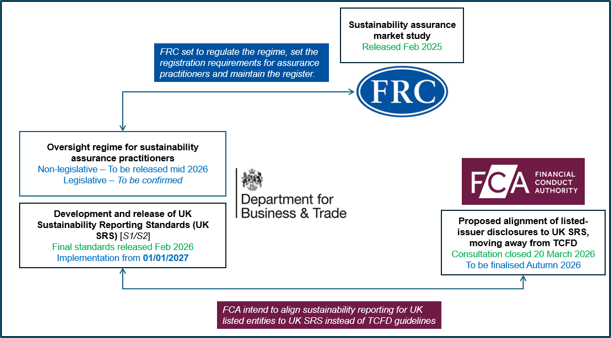

The UK landscape for sustainability reporting and assurance is undergoing significant transformation, driven by coordinated initiatives from the UK Government through the Department for Business and Trade (DBT), the Financial Reporting Council (FRC), and the Financial Conduct Authority (FCA). Together, they are trying to introduce clearer reporting standards and strengthened assurance expectations, while aiming to carve out a more coherent regulatory framework for sustainability related disclosures. The developments include:

- The FRC’s release of International Standard on Sustainability Assurance 5000 (ISSA 5000) for use;

- The Government’s issue of UK Sustainability Reporting Standards (UK SRS);

- The establishment of a voluntary oversight regime for sustainability assurance practitioners, operated by the FRC;and

- FCA proposals to align listed‑issuer sustainability reporting with UK SRS.

These changes aim to enhance credibility, comparability, and investor trust in sustainability reporting across the UK.

What is changing and why does it matter?

Market need for a stronger report, regulatory and assurance framework

The UK currently lacks a dedicated sustainability reporting framework, with companies currently reporting based primarily on Task Force on Climate-related Financial Disclosures (TCFD) standards. The FRC’s Assurance of Sustainability Reporting Market Study highlighted:

- A “growing preference among the largest companies to use the Big Four” for sustainability assurance, which could have implications for future choice in the market;

- Concerns about sustainability assurance market “immaturity”;

- Lack of regulatory clarity and “concerns over the consistency in the quality of the assurance provided”; and

- Risks to investor decision‑making due to a lack of consistent sustainability information.

These findings have prompted coordinated reform efforts across Government, the FRC and FCA.

The UK Government’s development of UK Sustainability Reporting Standards (UK SRS)

UK SRS has been developed based on the standards set by the International Sustainability Standards Board (ISSB), with the aim of ensuring standards adapted for the UK context are aligned with international approaches.

UK SRS S1 General Requirements for Disclosures of Sustainability-related Financial Information requires an entity to disclose information about its sustainability-related risks and opportunities that is useful to primary users of general-purpose financial reports in making decisions relating to providing resources to the entity.

UK SRS S2 Climate-Related Disclosures requires an entity to disclose information about its climate-related risks and opportunities that is useful to primary users of general-purpose financial reports in making decisions relating to providing resources to the entity, consisting of Scope 1, 2 and 3 disclosures. Scope 1 disclosures relate to direct greenhouse gas emissions that occur from sources that are owned or controlled by an entity, while Scope 2 disclosures relate to indirect greenhouse gas emissions from the generation of purchased or acquired electricity, steam, heating or cooling consumed by an entity. Scope 3 disclosures relate to indirect greenhouse gas emissions that occur in the value chain of an entity both upstream and downstream.

Both standards were finalised by the Government in February 2026. Adoption is currently voluntary for all companies. However, were FCA proposals to proceed, these standards would eventually apply to all listed companies.

The scope of UK SRS compliance may expand to other private entities as part of the Government’s broader modernisation of corporate reporting work, though what shape this might take is currently unknown – a consultation has been promised but, at the time of writing, the timetable for this is unclear.

The Government and FRC: A voluntary oversight regime for sustainability assurance providers

A voluntary FRC‑run oversight regime is being proposed by Government to be introduced mid‑2026. A key step is the establishment of a register of entities able to provide assurance over sustainability reporting. This register will be ‘profession agnostic’: both audit firms and non‑audit specialists can register. The intention is to improve quality, transparency, and competition in the sustainability assurance market, and to ensure the UK sustainability assurance market has a level playing field in terms of quality.

The register is expected to broadly align with EU CSRD subsidiary exemption requirements, enabling UK practitioners to provide assurance over UK parents of EU subsidiaries, over UK entities listed in EU member states, and over the consolidated group disclosures where an EU subsidiary has taken the exemption to provide local reporting and is included only in the UK consolidation.

This would be significant as it would support UK practitioners competing in Europe and helps UK headquartered groups avoid duplicative assurance costs. Currently, EU registered companies can only qualify for the CSRD exemption requirements if they are assured by a registered practitioner; the lack of a UK register means UK practitioners have had to transfer work to European arms, or UK parent companies have sought assurance services from EU practitioners.

Although registration will remain voluntary initially, there is scope for legislation to make registration mandatory in future.

The FCA: Alignment of listed-issuer disclosures

The FCA is focused on replacing current TCFD-aligned listing rules with UK SRS-aligned disclosure obligations and is consulting on the way forward. The FCA‘s intention is that listed companies must fully adopt UK SRS S2 Scopes 1 and 2 and then ‘comply or explain’ against the adoption of Scope 3 and the broader UK SRS S1 requirements.

It is anticipated UK SRS compliance will be required for listed companies in line with the following timeline, dependent on the outcome of the FCA consultation:

- UK SRS S1: Optional 2-year transitional relief from 1 Jan 2027, transitioning to comply or explain from 1 Jan 2029

- UK SRS S2 (Scope 1 & 2): Mandatory from 1 Jan 2027

- UK SRS S2 (Scope 3): Optional 1-year transitional relief from 1 Jan 2027, transitioning to comply or explain from 1 Jan 2028

It is also proposed that companies disclose:

- Whether they have a published climate transition plan; and

- Whether sustainability disclosures are externally assured, and by whom.

The consultation results are expected in Autumn 2026.

What this means in practice

Companies

- Anticipate increased expectations around governance, data quality, and transparency.

- Earlier adopters of UK SRS (from 2027) may benefit from smoother transition to mandatory disclosure requirements.

- The FRC oversight register should make it easier to identify credible sustainability assurance providers.

Assurance providers

- Registration intends to signal quality and market credibility which may involve compliance with standards such as ISSA (UK) 5000 and ISQM (UK) 1 – which may rule out smaller, independent boutique assurance firms.

- Smaller firms may face higher costs and capability gaps.

- Register aims to enhance access to EU‑related sustainability assurance work.

The UK market

- Aims for increased clarity and comparability strengthen the UK’s position as a hub for sustainable finance.

- Aims to align UK assurance market with global ISSB‑based reporting trends.

- Expected to support inward investment by improving trust in sustainability disclosures.