Building Trust in UK Business Through Improved Audit Quality

High-profile corporate collapses in the previous decade brought audit quality into the spotlight.

When Carillion and BHS failed, they shook public trust and market confidence. The response by audit firms and the regulator, the Financial Reporting Council (FRC), was a collective commitment to audit reform, to restore trust in the quality of Public Interest Entity (PIE) audit and strengthen UK capital markets.

Several years on, there has been tangible progress. Here are three significant developments reshaping the audit landscape:

- Strengthened corporate governance at audit firms. The 2022 Audit Firm Governance Code strengthened oversight of the largest audit firms. Independent Non-Executive Directors now play a more prominent role in representing the public interest, ensuring firms balance their audit and non-audit work with the right priorities.

- A clear separation between services. Led by the FRC, the UK’s four largest audit firms voluntarily separated their audit and non-audit practices. This operational separation has a clear aim: keeping audit teams focused on delivering high-quality Public Interest Entity (PIE) audit in the public interest, free from conflicting priorities.

- A new quality framework based on professional standards. The adoption of the International Standard on Quality Management (ISQM) gives firms a comprehensive framework for managing quality. It sets out clear responsibilities for designing, implementing, and operating quality management systems across all audit and assurance engagements.

Measuring what matters

Progress means little without measurement and audit transparency. The FRC’s annual Audit Quality Reviews (AQRs) provide that—they monitor audit quality across firms that audit Public Interest Entities and other significant organisations.

Using a risk-based approach, the FRC selects individual audits for inspection and assesses them across four categories:

- Good

- Limited improvements required

- Improvements required

- Significant improvements required

The FRC takes a risk-based approach to determine the areas reviewed on each individual audit. The focus is on areas that have a significant impact on an entity’s financial statements should they not be fairly stated and on which investors and users of financial reports may rely. In addition to these areas, the FRC reviewed risk assessments, audit planning and communications on all 2025 inspections.

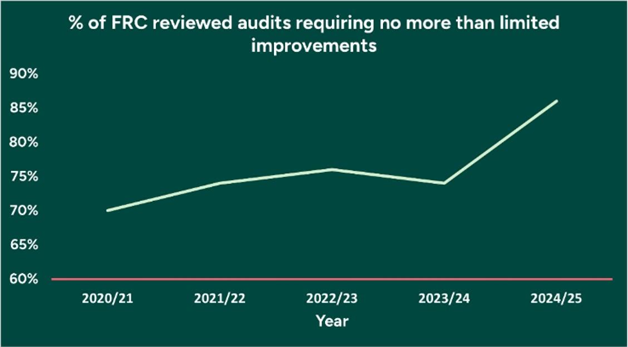

Results are encouraging

The 2025 AQR results show significant improvement in audit quality delivered by Tier 1 firms, with continuous progress over the past five years as seen below:

The 2024 CPIA Audit Trust Index reinforces the positive trend. Key stakeholders including audit committee chairs (94%) reported being satisfied with audit quality, along with 86% of finance directors and 77% of investors. These figures signal growing market confidence and public trust in audit.

But the work isn’t finished

These combined results are encouraging, yet there is still work to do, especially when the landscape is evolving at pace. Audit reform, technology, and sustainability reporting are reshaping the profession. The audit market of 2030 will look markedly different from today’s. Audit quality must remain a core foundation.

A shared responsibility across stakeholders

Here’s the crucial point: audit quality isn’t solely the responsibility of audit firms. Effective stakeholder engagement means everyone with a stake in audit has a role to play. Audit committees, management teams, regulators, investors, and standard setters all contribute to the quality of financial reporting standards and audit.

Strong audits require audit professionals to collaborate effectively. When directors provide timely, accurate information and engage constructively with their auditors, audit quality improves.

When audit committees ask challenging questions and maintain robust corporate governance oversight, the entire system strengthens. Sustaining the commitment to adapt to tomorrow’s challenges requires everyone to stay engaged.

What are your views on audit quality? Join the conversation by contacting the CPIA or follow our ongoing research into audit reform.